How Are Mutual Funds Taxed in FY 2020-21?

Table of Contents

How Mutual Fund Taxation Works: Type, Residency and Holding Period

Mutual funds are a great tool to build long term wealth. One can benefit from the experience of an expert team to invest their money and grow wealth. Investors understand the benefits of investing in financial assets and are actively allocating more money to such assets when compared to physical assets like real assets and commodities. No wonder the mutual fund industry has been growing at a massive pace. Let us now look at how these instruments are taxed and the changes in taxation after the union budget of 2020.

Mutual fund taxation is determined on the basis on three important parameters which are;

Types of Mutual Fund – Equity or Non-Equity Mutual Funds

All mutual funds that hold 65% or more in equity instruments are known as equity mutual funds. They include equity oriented hybrid funds which hold 65% or more in equity. The funds that don’t quality under these criteria are taxed as non-equity mutual funds.

Your Residential Status – Resident or Non-Resident Individual (NRI)

Resident individuals are taxed differently when compared to NRIs. The income tax department has a residency calculator to arrive at your residential status.

Holding Period – Short Term or Long Term

Equity Investments are considered as short term if held for less than 365 days i.e., 1 year and non-equity investments held for less than 3 years are taxed as short term holdings. The below table illustrates how mutual funds are taxed on the basis of the invested duration;

| Type of Fund | Short Term | Long Term |

|---|---|---|

| Equity Funds | Held for <12 months | Held for >12 months |

| Equity Oriented Hybrid Funds (>65% in Equity) | Held for <12 months | Held for >12 months |

| All Other Funds | Held for <36 months | Held for >36 months |

The below table summarizes the taxation of resident and NRI for different types of mutual funds held across different time horizons;

Mutual Fund Taxation Based on Residency, Type and Holding Period

| Equity & Equity Oriented Funds | Resident Individual | NRI |

|---|---|---|

| Short Term Capital Gains (STCG) | 15% | 15% |

| Long Term Capital Gains (LTCG) | 10% above 1 Lakh | 10% above 1 Lakh |

| Non-Equity Mutual Funds | ||

| Short Term Capital Gains (STCG) | Individual Tax Slab | Individual Tax Slab |

| Long Term Capital Gains (LTCG) | 20% with Indexation | Listed 20% With Indexation & unlisted 10% without indexation |

Tax on Mutual Fund Dividends

The union budget of 2020-21 abolished dividend distribution tax. Dividends are now taxed at the investor’s applicable tax rate. The budget also mandates Tax Deducted at Source (TDS) @ 10% for resident individuals if the dividend income is more than ₹ 5,000 in a financial year. For NRIs, the TDS is as follows;

| (TDS) for NRIs | STCG | LTCG |

|---|---|---|

| Equity & Equity Oriented Funds | 15% | 10% |

| Non-Equity Mutual Funds | 30% (Assuming Investor is in the highest tax bracket) | Listed 20% With Indexation & Unlisted 10% Without Indexation |

The biggest change in taxation is with respect to taxation of dividends. Prior to this year, dividends were tax free in the hands of the recipients, but now, they are taxed at the receiver’s end and at his applicable tax rate. For someone in the highest tax bracket, one could end up paying more than 42% taxes on the dividends declared.

Investors with a longer time horizon stand to gain if they move to growth option as it ensures that your wealth grows at a faster rate. The below illustration shows the additional returns generated under the growth option for an investor in the 30% tax bracket;

| Details | Dividend Option | Growth Option |

|---|---|---|

| Amount Invested @ Year 1 | ₹ 10,00,000 | ₹ 10,00,000 |

| Growth @ 10% | ₹ 1,00,000 | ₹ 1,00,000 |

| Dividend @ 25% | ₹ 25,000 | – |

| Tax on Dividend @ 30% | ₹ 7,500 | – |

| Gain @ end of Year 1 | ₹ 92,500 | ₹ 1,00,000 |

| Amount Invested @ Year 2 | ₹ 10,92,500 | ₹ 11,00,000 |

| Growth @ 10% | ₹ 1,09,250 | ₹ 1,10,000 |

| Dividend @ 25% | ₹ 27,313 | – |

| Tax on Dividend @ 30% | ₹ 8,194 | – |

| Gain @ end of Year 2 | ₹ 1,01,056 | ₹ 1,10,000 |

| Amount Invested @ Year 3 | ₹ 11,93,556 | ₹ 12,10,000 |

| Growth @ 10% | ₹ 1,19,356 | ₹ 1,21,000 |

| Dividend @ 25% | ₹ 29,839 | – |

| Tax on Dividend @ 30% | ₹ 8,952 | – |

| Gain @ end of Year 3 | ₹ 1,10,404 | ₹ 1,21,000 |

| Amount Invested @ Year 4 | ₹ 13,03,960 | ₹ 13,31,000 |

| Growth @ 10% | ₹ 1,30,396 | ₹ 1,33,100 |

| Dividend @ 25% | ₹ 32,599 | – |

| Tax on Dividend @ 30% | ₹ 9,780 | – |

| Gain @ end of Year 4 | ₹ 1,20,616 | ₹ 1,33,100 |

| Amount Invested @ Year 5 | ₹ 14,24,577 | ₹ 14,64,100 |

| Growth @ 10% | ₹ 1,42,458 | ₹ 1,46,410 |

| Dividend @ 25% | ₹ 35,614 | – |

| Tax on Dividend @ 30% | ₹ 10,684 | – |

| Gain @ end of Year 5 | ₹ 1,31,773 | ₹ 1,46,410 |

| Market Value @ end of Year 5 | ₹ 15,56,350 | ₹ 16,10,510 |

| Additional Return | ₹ 54,160 |

The above illustration makes it very clear that the growth option is best suited to grow wealth in the long run because of its tax efficiency.

The income tax department rewards you with preferential tax treatment if you stay invested for longer time horizons with lower tax rate for equity investments above one year and indexation benefits for debt investments held for more than 3 years. It should also be noted that long term gains up to ₹ 1,00,000 are exempt from taxes each financial year. Connect with a Fee Only Financial Planner to help you with your taxes.

Schedule a Call

Schedule a Call

Recent Blogs

Should You Invest Your EPF Withdrawal in Equity?

The Union labour ministry amended the EPF scheme on March 28 to allow members to withdraw non-refundable advances in view of the nation-wide lockdown.

Learn More →

How Are Mutual Funds Taxed in FY 2020-21?

Mutual funds are a great tool to build long term wealth. One can benefit from the experience of an expert team to invest their money and grow wealth.

Learn More →

Smart Investing During a Global Pandemic Crisis

The pandemic has affected more a million lives around the world and has destabilized the global economy.

Learn More →

The Real Cost of Opting for a Loan Moratorium

The COVID 19 virus has disrupted lives across countries and people are having a hard time.

Learn More →

Small Savings Schemes Now Offer Lower Returns

The finance ministry has sharply cut the interest rates on small savings schemes including the Public Provident Scheme (PPF), Post Office Term Deposits, National Savings Certificate among others.

Learn More →

How to Protect Your Personal Finances Right Now

The spread of Covid 19 has caused fear and panic among large populations across the world.

Learn More →

The Right Time to Invest During a Market Correction

We are all shaken, shaken by the ferocity of the fall in the stock markets. Never have we seen a correction of this magnitude in such a short period.

Learn More →

Why Stock Markets Will Remain Volatile?

The reason why stock markets fluctuate revolves around the theory of demand and supply. If more people want to buy a stock, its market price will increase.

Learn More →

6 Benefits of a Small House Over a Bigger One

A small house has various benefits. The foremost is pricing, For instance, a one BHK unit in upcoming locality near Manyata Tech Park in Bengaluru would come around Rs. 35 lakh verses Rs. 90+ lakh for a 3 BHK unit.

Learn More →

How Time, Patience & Persistence Build Rs.5 Crore Wealth

At 20, time is your biggest asset and starting early pays off handsomely. Like Einstein said, “Compounding is the eighth wonder of the world.

Learn More →

Personal Finance Mistakes: How People Mismanage Their Money

The most common mistakes people make is not having a financial plan.

Learn More →

3 Pillars of Successful Investing Every Investor Should Know

We long for happy retirement years and often have a list of to-dos. From going for vacations, pursuing hobbies or catching up with friends and family,

Learn More →

5 Tips for Happy Retirement and Financial Security

We long for happy retirement years and often have a list of to-dos. From going for vacations, pursuing hobbies or catching up with friends and family,

Learn More →

Essential Financial Tips Every Retiree in India Should Know

It’s a pleasant place to be as most retirees end up without having funds to take care of themselves.

Learn More →

Compare ETF and Index Fund Investment Options in India

Investing to secure your financial future is on your mind, but, you are likely to get overwhelmed to choose between the various investment instruments available.

Learn More →

Fixed Income Investments: Benefits, Types & Key Risks

Confused about fixed income investments? From bonds to T-bills, learn how each instrument works, key risks, and which one fits your financial goals.

Learn More →

What Is a Super Top-Up Health Insurance Policy and How Does It Work?

Base Policy and Super Top Up Policy are two commonly used options while taking Health Insurance. Health insurance is an important tool to safeguard your financial well-being against unexpected medical expenses. As medical treatments become more expensive

Learn More →

Basics of Public Provident Fund (PPF)

The Public Provident Fund (PPF) is a popular savings scheme introduced by the National Savings Institute of the Ministry of Finance in 1968.

Learn More →

Limited Pay vs Regular Pay — Which Life Insurance Premium Option Is Right for You?

Limited pay vs regular pay – it is easy to get confused between options for your life insurance premium payment. While Life insurance plays a crucial role in securing the financial future of your loved ones.

Learn More →

Everything You Need to Know About EPF Taxation in India

EPF does maintain its “EEE(exempt-exempt-exempt)” status but with certain conditions. “EEE” means the contributions towards EPF are exempt from income tax at the time of investment, interest earned on the contributions

Learn More →

What Should You Do With Your Life Insurance Policy?

In Indian families, pressure to buy traditional life insurance policies can be strong and multifaceted. Parents often play the “security card,” emphasizing the importance of safeguarding their child’s future and highlighting potential future burdens or painting a picture of an uncertain future without the policy.

Learn More →

Comprehensive Guide on Home Loan Overdraft Facility

Imagine a financial tool that combines the stability of a home loan with the flexibility of an overdraft account – that’s precisely what the Home Loan Overdraft Facility entails.

Learn More →

How to Choose from Different Gold Investment Options

Confused about gold investment options in India? From physical gold to SGBs, this guide compares costs, tax rules, and returns to help you make the right choice.

Learn More →

Index Funds - Advantages, Risks & Suitability

Index Funds are an investment instruments that are based on stock market indices like Sensex or Nifty. These funds are built using a pre-set basket of stocks from different sectors of the economy with predefined weights.

Learn More →

Direct Funds vs Regular Funds - Are Direct Mutual Funds better ?

Confused between direct and regular mutual funds? Compare expense ratios, NAV, and returns to find out which plan helps you grow your wealth long-term.

Learn More →

Debt Mutual Funds Taxation Changed: What Should You Do

Understand how Budget 2023 changed debt mutual fund taxation in India, removed indexation benefits and what it means for your investments compared to fixed deposits.

Learn More →

Emergency Fund - Essential Safety Net For Personal Finances

Emergency Fund can be your shield against financial storms. Life throws surprises, from unexpected medical bills to appliance breakdowns, emergencies can wreak havoc on your finances.

Learn More →

SSY Interest Rates, Tax Benefits, & Withdrawal Rules

Sukanya Samriddhi Yojana (SSY) is an initiative launched by the Government of India as part of its Beti Bachao, Beti Padhao campaign, (Save the Girl Child, Educate the Girl Child).

Learn More →

7 Types of Financial Ratios to Assess your personal finance & ways to improve them

Understanding the 7 types of financial ratios is a vital exercise that individuals should undertake to assess the state of their financial well-being.

Learn More →

What Should you do with your 401K Account if you Move Back to India

Moving back to your home country after years of working in the US is an exciting chapter. However, it also comes with its own set of financial considerations, especially when it comes to your US retirement savings.

Learn More →

What Are ULIP Charges and How Do They Work

Know about ULIP charges in India covering mortality, policy admin, switching, surrender, and guarantee fees to help you decide if ULIP is worth investing in.

Learn More →

Key Features of NPS (National Pension Scheme)

The National Pension Scheme is a government-sponsored retirement savings plan introduced in India in 2004. It provides a structured approach for individuals to build a retirement fund by making regular contributions.

Learn More →

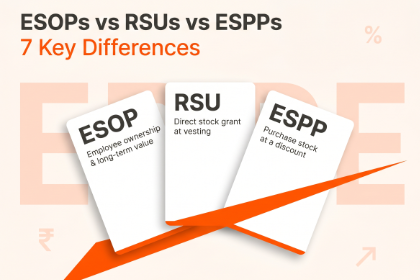

ESOPs vs RSUs vs ESPPs - Understand the 7 key differences

In today's competitive Indian job market, companies are increasingly turning to equity compensation plans to attract and retain top talent.

Learn More →

12 Risks of Investing ESOPs/RSUs/ESPPs

Imagine your future self, financially secure thanks to a hefty chunk of your employer's stock, a reward for your dedication and hard work.

Learn More →

What Should You Do With Your Life Insurance Policy Decision

Confused about what should you do with your life insurance policy? In Indian families, pressure to buy traditional life insurance policies can be strong and multifaceted.

Learn More →

5 Proven Ways to Build Stable Post Retirement Income in India

Retirement brings major changes in income and life. Investments and savings can help you meet your needs, but a steady income is still essential for daily expenses and regular cash flow.

Learn More →

12 Must Follow Financial Practices Before Moving Abroad

When one is leaving the familiar shores of India for a new life abroad, it may be both exciting and daunting. It's exciting to pack up your bags and head out on a new adventure, but one of the biggest challenges you will face is getting used to a new financial environment.

Learn More →

5 Reasons to Prefer a Fee-Only Financial Planner in India

The term "financial planner" is used often and very loosely. In India, many people call themselves financial planners, the insurance agent, the mutual fund distributor,

Learn More →

How do Financial Planners & Advisors Get Paid in India?

SEBI (Securities Exchange Board of India), with its latest amendments to Registered Investment Adviser (RIA) Regulations, mandates that all registered financial planners can charge only on two bases. A Financial Planner can either charge a fee for financial planning or earn from distribution of financial products.

Learn More →

How to Choose The Best Financial Advisor In India

If you are confused about how to choose the best financial advisor in India, you can thank the Securities Exchange Board of India (SEBI).

Learn More →

Income Tax Deductions & Exemptions: Full Guide for Taxpayers

Salaried employees make up a big part of taxpayers, and their tax contributions matter. Income tax deductions provide various chances for them to save money on taxes.

Learn More →

5 Differences Between Regular Mutual Funds and Direct Mutual Funds

In today's dynamic financial landscape, mutual funds have become a popular investment option in India. Whether you're a seasoned investor or just starting, the sheer number of options and the constant market fluctuations can feel daunting.

Learn More →

6 Reasons to Review Your Financial Plan for Better Financial Health

Reviewing your financial plan matters as much as using a trusted navigation system. When you move forward without regular reviews, you risk heading in the wrong direction.

Learn More →