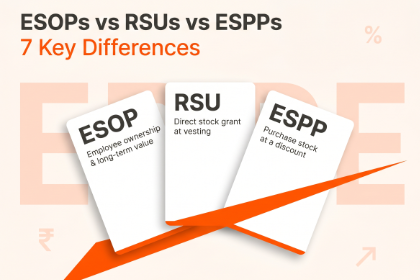

ESOP, RSU & ESPP Risks Every Employee Should Know

Table of Contents

Is Your Equity Compensation Putting Your Wealth at Risk?

Imagine your future self, financially secure thanks to a hefty chunk of your employer's stock, a reward for your dedication and hard work. Sounds enticing, right? Employee Stock Ownership Plans (ESOPs), Restricted Stock Units (RSUs), and Employee Stock Purchase Plans (ESPPs) are increasingly popular ways for companies to attract and retain talent by offering ownership. But before diving headfirst into this equity pool, it's crucial to understand the Risks of investing in ESOPs/RSUs/ESPPs.

Let’s explore the various risks associated with having high exposure to your company's stock through ESOPs, RSUs, or ESPPs. We will dive into the financial, emotional, and career-related implications, empowering you to make informed decisions about your equity compensation.

12 Risks of investing in ESOPs/RSUs/ESPPs

The Double-Edged Sword of Concentration Risk:

One of the major Risks of investing in ESOPs/RSUs/ESPPs is increasing concentration towards a single stock. While owning a piece of a successful company can be rewarding, there's no guarantee of future success. Putting all your eggs in one basket is risky. Relying heavily on company stock can lead to concentration risk, where a significant portion of your wealth is tied to the performance of a single company. If the company encounters financial difficulties or its stock price declines sharply, your financial well-being could be severely impacted.

Lack of Diversification:

ESOPs, RSUs, and ESPPs often result in a lack of diversification in an individual's investment portfolio. Diversification is key to mitigating this risk. Consider spreading your investments across different asset classes to balance your portfolio.

The Volatile Dance of the Market:

The stock market is a roller coaster ride, and your company's share price might not always go up. Economic downturns, industry disruptions, and unforeseen events can cause stock prices to plummet, potentially wiping out your hard-earned gains. Remember, high potential returns come with high potential risks. Company stock can be highly volatile, especially for smaller or younger companies. High volatility can lead to large swings in the value of your equity compensation, causing stress and uncertainty.

Regulatory & Tax implication:

Exercising stock options or receiving RSUs triggers taxable events. Be prepared for potential capital gains taxes and ordinary income taxes depending on the type of equity compensation and your exercise strategy. There are complex tax implications associated with ESOPs, RSUs, and ESPPs. Changes in tax laws or regulations could affect the after-tax value of your equity compensation, potentially reducing its effectiveness as a wealth-building tool. Consulting a financial advisor can help you navigate the tax implications and minimize your tax burden.

The Waiting Game:

ESOPs and RSUs typically come with vesting schedules and other restrictions that limit your ability to sell the shares immediately. This lack of liquidity can be problematic, especially if you need cash for unexpected expenses, meeting life goals or capture investment opportunities. This creates a lock-in effect, tying your financial fortunes to the company's performance for a set period. While it promotes long-term commitment, it also limits your liquidity and flexibility. Carefully evaluate your financial needs and risk tolerance before relying heavily on illiquid assets.

The Emotional Rollercoaster:

Owning a significant portion of your company's stock can be emotionally draining. Stock price fluctuations can trigger anxiety and stress, affecting your well-being. It's essential to separate your emotional attachment to the company from your financial decisions. Don't let stock performance dictate your mood or career choices.

The Career Crossroads:

High equity ownership can make leaving your company a difficult decision. The potential loss of unvested shares or favourable exercise prices can create a golden handcuff effect, limiting your career options. Ensure your career path aligns with your aspirations, not just your stock options. Don't sacrifice your professional growth for an uncertain financial future.

Employment Risk:

If your salary, bonuses, and equity are all tied to the same employer, your financial well-being may become overly dependent on your continued employment with the company. A company downturn could impact your income, savings, and retirement plans simultaneously. If you lose your job or the company faces financial difficulties leading to layoffs, not only could you lose your income, but the value of your equity compensation may also decline.

Market Risk:

Even if the company performs well, broader market forces can still impact the value of its stock. Economic downturns, industry-specific challenges, or geopolitical events can all affect stock prices, regardless of the company's individual performance.

Overvaluation Risk:

Employees may overestimate the future performance of their company's stock, leading them to allocate too much of their wealth to equity compensation. If the stock is trading at an inflated valuation, there's a risk of a correction that could result in significant losses.

Incentive Misalignment:

In some cases, the interests of employees may not align perfectly with those of shareholders. For example, management may prioritize short-term stock price performance to boost their own compensation, potentially at the expense of long-term value creation.

Complexity & Monitoring Requirements:

Managing a portfolio heavily concentrated in company stock requires careful monitoring and periodic rebalancing to ensure it remains aligned with your financial goals and risk tolerance. This can be time-consuming and may require expertise that not all individuals possess.

Beyond the Risks of investing in ESOPs/RSUs/ESPPs : Making Informed Choices

Understanding the risks of investing in ESOPs/RSUs/ESPPs doesn't negate the potential benefits of ESOPs, RSUs, and ESPPs. They can be powerful tools for wealth creation and employee engagement. The key is to approach them with awareness and caution. Here are some tips:

Diversify your portfolio : Don't let your company stock become your sole financial focus. Analyse the risks of investing in ESOPs/RSUs/ESPPs and consider systematic selling of vested shares and reinvesting the proceeds in a diversified portfolio across different asset classes, industries, and sectors. This reduces concentration risk and mitigates exposure to potential declines.

Target Dates & Profit Goals : Set realistic profit targets for selling shares based on market research and company performance. Utilize time-based approaches like target dates if appropriate for your financial goals.

Seek professional advice : Consult a financial advisor to understand the tax implications, investment strategies, and risk management techniques relevant to your situation.

Don't let emotions dictate decisions : Make rational financial choices based on research and analysis, not fear or hope.

Prioritize your career : Don't let stock options hinder your professional growth. Explore opportunities that align with your aspirations, even if they mean leaving your current company.

Stay informed : Keep yourself updated on your company's financial health and industry trends to make informed decisions about your equity compensation.

Remember, there's no one-size-fits-all solution. Carefully assess your risk tolerance, financial goals, and career aspirations before making decisions about your company stock. By identifying the potential risks of investing in ESOPs/RSUs/ESPPs and making informed choices, you can leverage ESOPs, RSUs, and ESPPs to your advantage and build a secure financial future. Book your free consultation call today to discuss your financial goals and create a diversified portfolio that aligns with your risk tolerance. Book a Free Introductory Call