Home

Services

Investment Planning

Retirement Planning

NRIs Financial Advisory

Financial Planning for Couples

Financial Planning for Women

About

Blogs

Testimonials

SEBI Disclosures

Beware of Imposters

Pricing

Schedule a Call

Home

Blog

Latest Blogs on Financial Planning & Wealth Growth

Expert Financial Advisory & Wealth Planning Blogs

The Right Time to Invest During a Market Correction

Read More

Why Stock Markets Will Remain Volatile?

Read More

Limited Pay vs Regular Pay — Which Life Insurance Premium Option Is Right for You?

Read More

Base Policy & Super Top Up Policy

Read More

Home Loan Overdraft Facility — Everything You Need to Know Before You Apply

Read More

How to Choose from Different Gold Investment Options?

Read More

Index Funds - Advantages, Risks & Suitability

Read More

Direct Funds vs Regular Funds - Are Direct Mutual Funds better?

Read More

SSY Interest Rates, Tax Benefits, & Withdrawal Rules

Read More

7 Types of Financial Ratios to Assess your personal finance & ways to improve them

Read More

What Should you do with your 401K Account if you Move Back to India

Read More

5 Different Charges in ULIP Plan!

Read More

Key Features of NPS (National Pension Scheme)

Read More

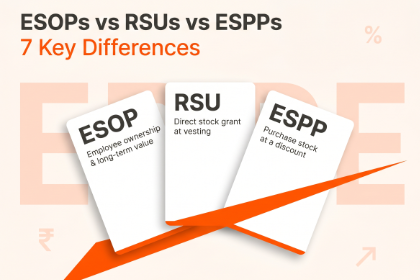

What Indian Employees Must Know about ESOPs Vs RSUs Vs ESPPs

Read More

12 Risks of Investing ESOPs/RSUs/ESPPs

Read More

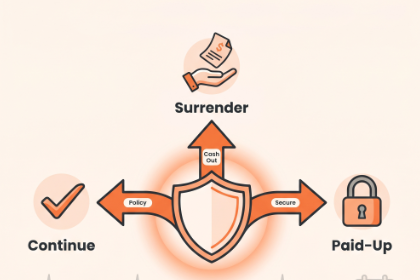

What Should You Do With Your Life Insurance

Read More

12 Must Follow Financial Practices Before Moving Abroad

Read More

5 Reasons to Prefer a Fee-Only Financial Planner for Your Wealth

Read More

Income Tax Deductions & Exemptions: Full Guide for Taxpayers

Read More

5 Proven Ways to Build Stable Post Retirement Income in India

Read More

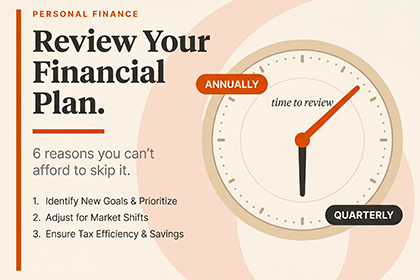

6 Reasons You Should Review Your Financial Plan Regularly

Read More

How to Choose The Best Financial Advisor In India

Read More

How do Financial Planners & Advisors Get Paid in India

Read More

SEBI's mandatory disclosure requirement

View More