What Are the Different ULIP Charges & Types in India?

Table of Contents

How ULIP Charges Impact Your Investment Returns?

ULIPs, or Unit Linked Insurance Plans, combine investment and insurance in one product. They offer life cover and let you benefit from the Various investment products like stocks, bonds, or commodities.

These plans are offered by life insurance companies, where your payments are termed as 'premiums'. ULIPs are primarily structured like insurance plans. Part of premium goes towards life insurance & part of your premium goes towards the investment component, which includes Investments in equity, debt etc. Professional fund managers oversee these investments. You have the flexibility to switch between different types of funds to customize your ULIP plan according to your preferences.

ULIPs started in 1971 with the Unit Trust of India (UTI) and later by Life Insurance Corporation (LIC) in 1989, they have evolved significantly.

Lock In Period of ULIP Policy

A key feature of ULIP policies is the lock-in period, which typically lasts for a minimum of five years. During this time, investors are unable to withdraw funds or surrender the policy without penalties.

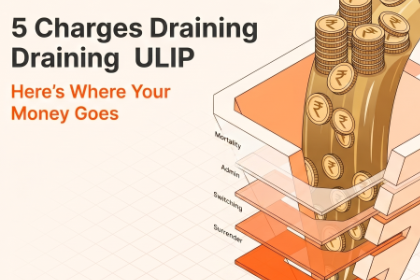

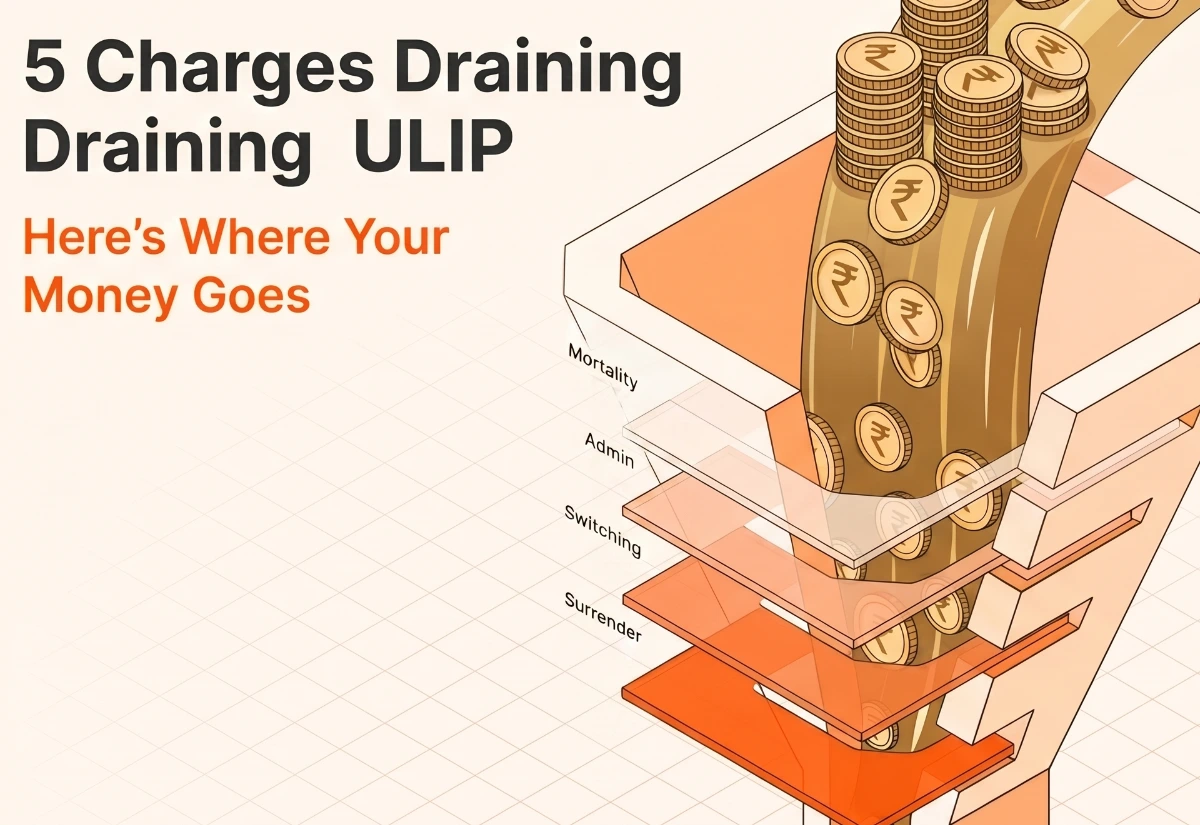

Types of ULIP Charges in ULIP

ULIPs can come with a variety of fees, so it is important to understand what you are paying for. Here is a breakdown of some common ULIP charges:

Premium Allocation Charges:

Before your ULIP investment is apportioned between insurance and investment components, charges are deducted upfront from your premium payment. These premium allocation charges cover the insurer's expenses for underwriting, selling the product, commissions, medical tests, and other initial costs associated with issuing the policy. Typically, insurance companies deduct a fixed percentage, which can vary between 5% to 30% of the premiums paid. For Instance, if the premium allocation charge is 10%, on a premium of Rs. 1,20,000, Rs. 12,000 would be deducted towards charges, leaving Rs. 1,08,000 to be invested. This is a fixed fee that can vary across the years. This is usually high in the first year and reduces subsequently.

Mortality Charges:

Life insurance companies charge a mortality fee to provide life cover for you. This fee is based on the below parameters:

- Your age : Generally, younger folks pay less because they are statistically likely to live longer.

- Your health : If you are healthy, the company figures you are less likely to need the payout soon, so they charge you less.

- How much money your loved ones get : The bigger the payout, the more the company risks, so the fee goes up.

- How long the plan lasts : Longer plans mean the company takes on the risk of you passing away for a longer period, so the fee might be higher.

The company is basically betting you will live for a while. The stronger the bet looks for them (young, healthy, smaller payout, shorter plan), the lower your fee.

Policy Administration Charges:

Policy administration charges in a Unit Linked Insurance Policy (ULIP) are a monthly fee designed to cover the administrative costs associated with managing the policy. These charges can either be fixed or variable and typically encompass expenses such as policy maintenance, paperwork, record-keeping, and premium notifications.

The policy administration charges are usually at 2.25% per annum but capped at ₹500 per month whichever is lower. Any revision of these charges requires prior approval from IRDAI.

Switching Charges:

ULIPs let you invest your money in different types of instruments, like stock funds (equity) or bond funds (debt). You can usually switch your money between these funds. However, some insurers might charge you a fee for each switch you make.

Imagine ULIP funds like different baskets for your eggs. You can move your eggs (investment) between baskets (funds) but there might be a small fee for each move.

For instance, if you decide to switch from an equity fund to a different fund, such as debt or hybrid, the insurer may impose a switching charge.

Surrender Charges:

A surrender charge, also referred to as a discontinuance charge, applies when a unit linked insurance plan (ULIP) is terminated before its five-year lock-in period. This charge, typically a percentage of the fund value and premiums paid or a fixed amount, aims to recover the insurer's initial acquisition costs. Upon surrender, the remaining fund value, reduced by these charges, is transferred to a discontinued policy fund where it accrues interest until the end of the lock-in period. Post-lock-in, both the fund value and accumulated interest can be withdrawn.

Guarantee Charges:

Normally, ULIP returns depend on how the market performs. Just like the weather affects your picnic plans, market ups and downs can impact your ULIP returns.

Some ULIPs offer a guaranteed minimum return after a set time. For example, a plan might guarantee 8% returns after 10 years. This means you will get at least 8% growth on your investment, regardless of market conditions. It is like having a safety net – even if the market performs poorly, you will still see some growth.

There is a catch, though! The insurance company charges you extra (guarantee charge) for making this promise. It is like paying a bit more for peace of mind. You get a guaranteed minimum return, but you also pay a fee for that security.

Fund Management Charges:

ULIPs involve investing your money in different markets. To manage your investment and make sure your money grows, the insurance company charges a fee called a fund management charge. This fee covers the costs of professional managers who look after your investment. In India, the insurance regulator limits this fee to a maximum of 1.35% per year, so you know it will not be excessive.

Top up Charge:

Imagine ULIPs like a bucket where you invest your money. Top-up is like adding extra money to your bucket whenever you have some savings. Think of it like planting more seeds - the more you plant, the bigger the harvest you might get later.

It is important to note that insurance companies might charge a small fee for each top-up you make. This fee is like a service charge for handling your additional investment.

Rider Charges:

ULIPs offer some extra protection you can tack on, called riders or add-on covers. These are like boosters for your insurance coverage, but they cost extra. Think of it like adding sprinkles to your ice cream - they make it more exciting, but you pay a little more for them. Each insurance company offers different rider options, so be sure to check what they are and how much they cost before adding them to your ULIP plan.

Miscellaneous Charges:

ULIPs come with a variety of miscellaneous charges beyond the core investment fees. These are typically smaller fees applied for specific actions you take with your policy. Think of them like small handling costs. Examples include fees for:

- Changing your premium payment mode (e.g., monthly to annually)

- Updating your beneficiary information

- Making excess fund switches beyond a certain allowed number

Considering ULIPs for Investment: Is It a Wise Choice?

ULIPs (Unit Linked Insurance Plans) are often pitched as a one-stop shop for both insurance and investment needs. But before you jump in, consider the downsides:

Higher Fees, Half the Potential:

ULIPs layer insurance costs on top of investment charges. You could end up paying more than for separate insurance and investment products, and these fees can significantly eat into your potential returns. Imagine you invest Rs. 10,000, but ULIP charges take a chunk out, leaving you with less money to grow in the market. Would not you rather have that full Rs. 10,000 working for you?

Uncertain Returns:

ULIPs often show high potential returns, but these figures do not factor in all the fees. Your returns might be much lower. Additionally, market fluctuations can significantly impact your investment portion.

Locked In, Limited Out:

ULIPs come with a lock-in period, typically 5 years. During this time, accessing your money can be difficult and incur additional charges. This inflexibility might not suit your financial needs.

Insurance Needs an Expert, Investments Need Another:

Financial advisors specializing in insurance and investments have different skillsets. A ULIP salesperson might not be the best advisor for both aspects of your financial plan.

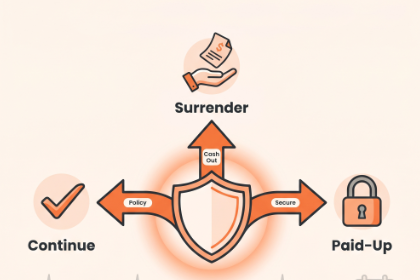

Managing Your Existing ULIP Policy: Steps to Take Now

Thinking of cashing out your ULIP investment? It is important to understand what that means for your money. Here is a breakdown:

Surrendering the ULIP plans before the lock-in period:

You have the option to surrender the policy before the lock-in period ends, though the life cover will terminate upon surrender. However, the surrender value, which is based on the investments, is paid out only after the five-year lock-in period.

The surrender value of a ULIP policy is determined not solely by the fund value at the surrender date, but also by deducting applicable discontinuation charges. This value varies based on the insurer's specific policy conditions, incorporating factors such as the ratio of insurance to investment, mortality charges, and fund management fees.

After deducting discontinuation charges, the money left from your investment fund is moved to a fund called the Discontinued Policy (DP) fund. This fund stays active until your ULIP completes its lock-in period. A small fee, up to 0.5% of the fund's value, is charged for managing the DP fund during this time.

The Discontinued Policy (DP) fund will accrue some kind of interest annually until the ULIP is paid out after the lock-in period. The specific interest rate is subject to IRDAI regulations and may vary.

Another important aspect to consider is the tax implications of surrendering a ULIP. If you surrender a ULIP policy before the lock-in period, any tax deductions previously claimed will be treated as income and taxed according to your income tax slab. Additionally, the surrender value will be subject to Tax Deducted at Source (TDS).

Surrendering the ULIP plans After the lock-in period:

After the five-year lock-in period ends, ULIPs generally become more flexible in terms of accessing your money. Here is the good news: there are typically no surrender charges if you decide to withdraw your funds entirely. This means you get back the full account value (minus any small ongoing fees) minus any unpaid premiums. It is like finally having unrestricted access to your investment after the initial commitment period.

Why Mixing Insurance and Investments Might Be a Recipe for Regret

Remember: Insurance protects your loved ones in case of unforeseen events. Investments aim to grow your wealth over time. Mixing these goals in a ULIP might not be the most effective strategy. Consider exploring separate term insurance (for pure protection) and mutual funds (for potentially higher returns and more control) for a potentially more robust financial plan.

Term Insurance : Provides pure life insurance coverage at a lower cost, freeing up money for dedicated investments. Read here to understand how much life insurance you should get?

Mutual Funds : Offer a wider range of investment options with potentially higher returns and more control over your portfolio.

Are you making the most of your ULIP investments? Is It a good decision to invest in ULIP? Whether you are just starting out or have an existing policy, understanding the charges associated with ULIPs can significantly impact your returns. Let us work together to assess your current ULIP portfolio, identify opportunities for optimization, and strategize for future growth. Take the first step towards financial empowerment— Schedule a free consultation calls today and let us unlock the full potential of your ULIP investments! Book a Free Introductory Call