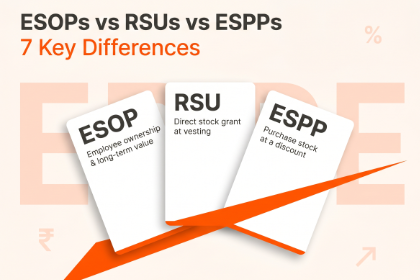

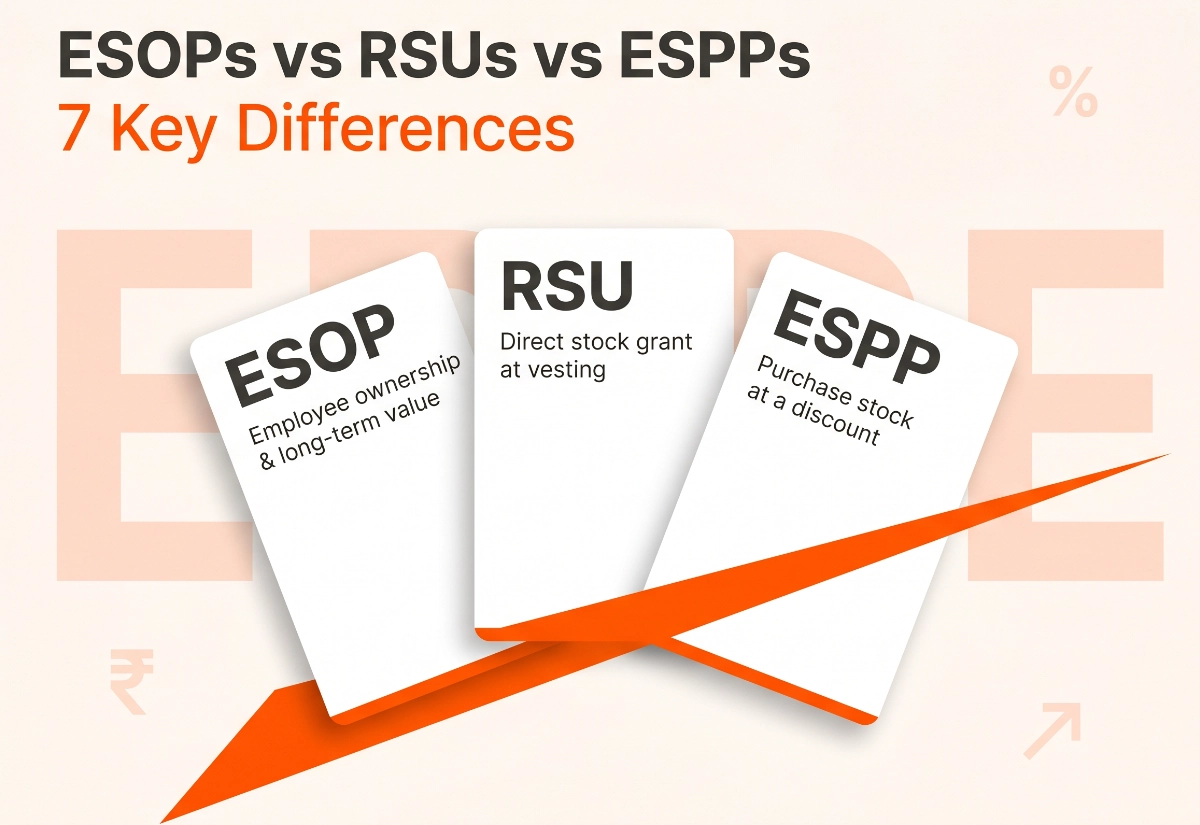

ESOPs vs RSUs vs ESPPs - Understand the 7 key differences

Table of Contents

Tax Implications of ESOPs RSUs & ESPPs in India

In today's competitive Indian job market, companies are increasingly turning to equity compensation plans to attract and retain top talent. These plans, like Restricted Stock Units (RSUs), Employee Stock Purchase Plans (ESPPs), and Employee Stock Option Plans (ESOPs), offer employees a stake in the company's success, aligning their interests with organizational goals. However, understanding the key differences between ESOPs vs RSUs vs ESPPs , their benefits, drawbacks, and, most importantly, the tax implications of these plans in India is crucial for making informed decisions.

A) Employee Stock Ownership Plans (ESOPs)

An Employee Stock Ownership Plan (ESOP) is a program that offers employees ownership interest in the company, usually as a part of their remuneration package. These shares are typically granted over time, encouraging employees to stay with the company.

The ESOP cycle:

The ESOP cycle outlines the journey of an employee stock option plan, from grant to potential profit (or loss) for the employee. Here's a breakdown of the key stages:

1. Grant Date:

The company grants you the right, but not the obligation, to purchase a specific number of shares of company stock at a predetermined price (exercise price) within a set timeframe (vesting period).This formalizes the agreement and sets the following key terms:

- Number of stock options granted

- Exercise price (price you can buy the shares at)

- Vesting schedule (when you gain ownership rights)

- Expiry date (deadline to exercise the options)

2. Vesting Period:

This is the waiting period before you officially own the offered shares. You must remain employed with the company for this time to be eligible to exercise your options. Vesting can be:

- Cliff Vesting : All options vest at once after a specific period (e.g., 4 years).

- Graded Vesting : Options vest gradually over time in portions (e.g., 25% each year for 4 years).

3. Vesting Date(s):

Once the vesting period(s) elapses, you gain ownership rights over the vested portion of your options. This is when you can decide whether to exercise them.

4. Exercise (Optional):

This is your decision point. You can choose to:

- Exercise : Purchase the shares at the predetermined exercise price. You'll need to pay this upfront cost to acquire ownership.

- Don't Exercise : Let the options expire if you don't believe the stock price will appreciate or don't have the funds to exercise.

Decision Factors for Exercising:

Exercise Price vs. Fair Market Value : If the fair market value (current stock price) is higher than the exercise price, there's potential profit by exercising and selling the stock later.

Financial Situation : You'll need to pay the exercise price upfront, so consider your financial readiness.

Market Outlook : Projecting the stock's future value can help you decide if exercising is worthwhile.

Holding or Selling (if exercised):

Once you own the shares (exercised), you can choose to:

- Hold : Keep the shares in hopes of future price appreciation.

- Sell : Sell the shares on the open market to capture any gains.

Taxation At Exercise:

Taxes are typically due when you exercise. The difference between the market price of the shares on the exercise date and the exercise price is taxed as a perquisite under 'Income from Salaries'.

B) Restricted Stock Units (RSUs)

RSUs stands for Restricted Stock Units. It's a form of equity compensation offered by companies to employees.

The RSU cycle:

The RSU cycle is a simpler process compared to ESOPs, but it's still important to understand the different stages:

1. Grant Date:

This is the date your employer awards you RSUs. They'll specify:

- Number of RSUs granted

- Vesting schedule (when you gain ownership)

2. Vesting Period:

Similar to ESOPs, you need to wait for this period to elapse before you officially own the underlying shares represented by the RSUs. Vesting can be:

- Cliff Vesting : All RSUs vest at once after a specific period.

- Graded Vesting : RSUs vest gradually over time in portions (e.g., 25% each year).

3. Vesting Date(s):

Once the vesting period is over, you gain ownership of the vested RSUs. These become actual shares of company stock. There's no option to decide here. Unlike ESOPs, RSUs automatically convert to company shares upon vesting.

Holding or Selling:

Now that you own the shares:

- Hold : Keep the shares in your brokerage account and potentially benefit from future price appreciation.

- Sell : Sell the shares on the open market to capture any gains (tax implications apply).

Taxation At Vesting:

The main taxable event in the RSU cycle is vesting. The market value of the shares on the vesting date is taxed as a perquisite under 'Income from Salaries'. Your employer may withhold taxes from the vested shares to cover your income tax liability based on the fair market value of the shares on the vesting date.

C) Employee Stock Purchase Plan (ESPP’s)

ESPP stands for Employee Stock Purchase Plan. It's a program that allows employees to buy shares of their company's stock at a discounted price, typically through payroll deductions.

The ESPP Cycle:

The ESPP cycle involves payroll deductions, periodic stock purchases, and potential ownership benefits for employees. Here's a breakdown of the key stages:

1. Enrollment Window:

This is the designated period when employees can choose to participate in the ESPP.

2. Election Period (or Offering Period):

If you decide to participate, you'll specify a contribution amount to be deducted from your paycheck throughout this period. This contribution will be used to purchase company stock on your behalf. The election period can be:

- Consecutive : One continuous period throughout the year.

- Overlapping : Multiple enrollment periods within a year, potentially with different purchase prices due to the staggered nature.

3. Payroll Deduction:

During the chosen election period, your employer will automatically deduct your designated contribution from your paycheck.

4. Purchase Date:

This is the pre-determined date on which the company uses the accumulated contributions from employees to buy company stock at a discount (typically 5-15% off market value). There can be multiple purchase dates within a year depending on the ESPP design.

5. Stock Allocation:

After the purchase date, the company allocates the purchased shares proportionally based on each employee's contributions. You officially become a shareholder.

Important Considerations:

Discount Window : The ESPP offers a chance to buy shares at a discount, but the purchase is locked in until the purchase date.

Contribution Limits : There may be limits on how much you can contribute to the ESPP per paycheck or per year.

Holding Period : Some ESPPs might require you to hold the shares for a certain period before selling them.

Holding or Selling:

Sell :

- Capture the discount benefit immediately (difference between market price and purchase price).

- Diversify your investments (don't put all eggs in one basket).

Hold :

- Potentially benefit from future stock price appreciation.

- Maintain ownership stake in your company (potentially motivating).

Taxation At Purchase:

The discount offered on the stock is taxed as a perquisite under 'Income from Salaries'. The difference between the purchase price and the fair market value on the date of purchase is taxable.

Tax collected at source Under LRS for International Equity Investments:

As of today, June 6, 2024, the rules regarding TCS (Tax Collected at Source) for international equity investments under the Liberalised Remittance Scheme (LRS) have changed from what they were in October 2023.

You can remit up to ₹7 lakh per financial year for international equity investments without any TCS. If your total remittance for international equity investments exceeds ₹7 lakh in a year, TCS will apply to the amount exceeding the limit. This applies to all investments exceeding ₹7 lakh, including stocks, mutual funds, and ETFs in foreign markets.

This TCS is not an additional tax. It's deducted upfront and can be adjusted against your future tax liability when you file your income tax return. The above information applies to individual LRS transactions. There might be different rules for corporate remittances.

Taxation At Sale of ESOPs vs RSUs vs ESPPs:

In case of International Equity & unlisted Indian Equity : Gains from the sale of ESOP shares are subject to capital gains tax. If held for more than 24 months, they are treated as long-term capital assets and taxed at 20% with indexation benefits. Short-term capital gains are taxed at the applicable income tax slab rates.

Incase of listed Indian equity : Short-term capital gains tax (15%) applies if the shares are held for less than a year. If shares are held above one year then Long-term capital gains upto Rs. 1 lakh are exempt from tax, with any gains above this threshold taxed at a concessional rate of 10% (without indexation).

ESOPs vs RSUs vs ESPPs

All three equity compensation plans – ESOPs vs RSUs vs ESPPs – come with a significant drawback called concentration risk. This refers to the risk of having a large portion of your net worth tied to a single asset – your employer's stock. Equity compensation plans can be a great way to share in your company's success, but it's crucial to manage concentration risk by diversifying your investments and having a well-rounded financial plan.

Refer to the blog to understand the risks of investing in ESOPS/RSUS/ESPPS

ESOPs vs RSUs vs ESPPs provide valuable opportunities for employees to participate in the ownership and success of their companies. Each plan has unique benefits, drawbacks, and tax implications. Understanding these details helps employees make informed decisions and maximize the financial benefits of their compensation packages. Unsure how RSUs, ESPPs, and ESOPs fit into your financial plan? Schedule a consultation with our financial advisors to understand how these equity compensation plans can impact your overall financial goals and develop a personalized strategy to maximize their benefits. Book a Free Introductory Call